Can You Finance MBBS Abroad With a Loan?

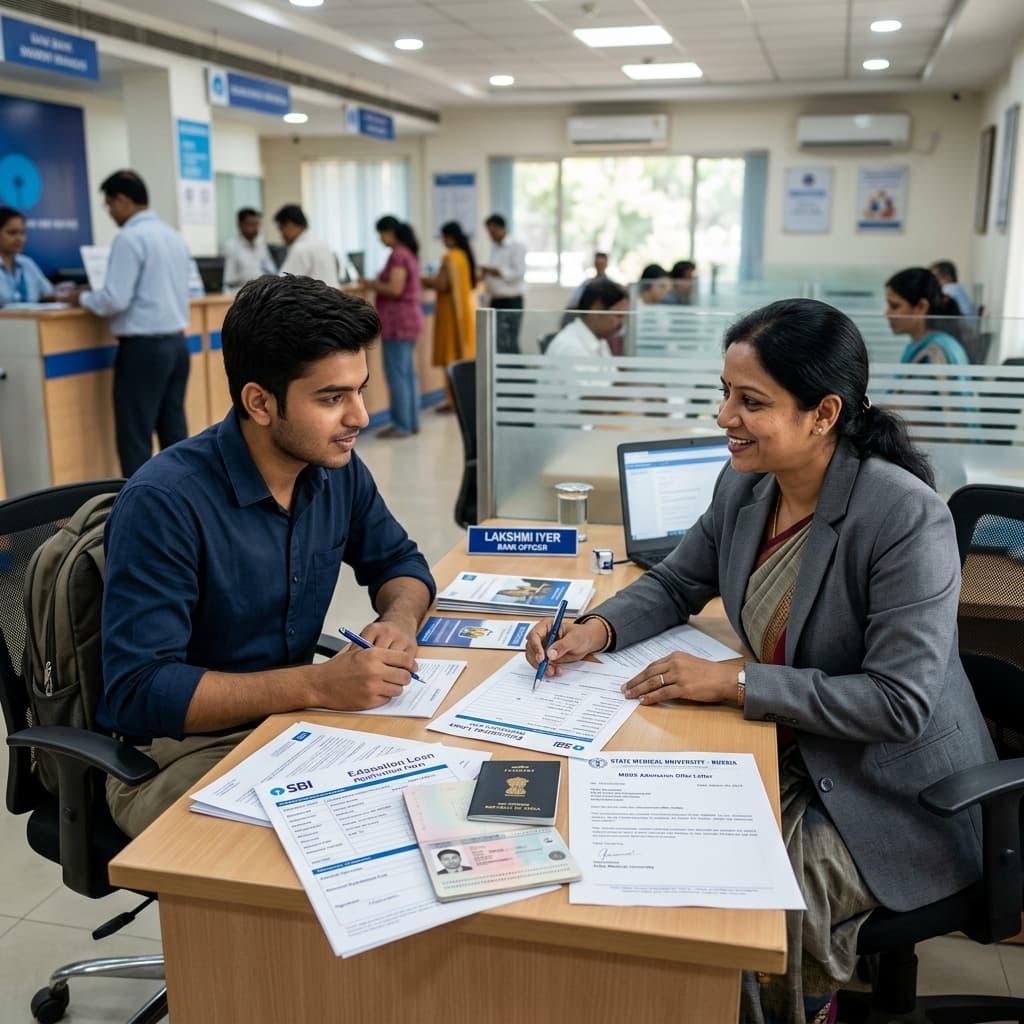

Yes — education loans for MBBS abroad are available from both public sector banks and private lenders in India. However, there are specific conditions that most families discover only after sitting across the table from a bank officer.

This guide explains exactly how education loans work for MBBS abroad: which banks offer them, how much they lend, what security they require, how interest accrues during the course, and the documents you genuinely need. No generic advice — specific, actionable information.

Who Qualifies for an Education Loan for MBBS Abroad?

To be eligible for an education loan for MBBS abroad, you need to meet these criteria:

- NMC-recognized university: The bank will verify this. Most public sector banks require the university to appear on the NMC approved list. If your university is not NMC-recognized, most banks will decline the loan (a signal you should also use to question the university choice itself)

- Valid NEET score: Many banks now require NEET qualifying proof for MBBS abroad loans, aligned with NMC rules

- Indian citizenship: Standard for domestic education loans

- Co-applicant (parent or guardian): Required for all student education loans in India; the co-applicant's income and credit history are assessed

- Collateral (for loans above ₹7.5–10L): Most MBBS abroad loans exceed this threshold, so collateral is standard

Bank-by-Bank Overview

SBI (State Bank of India)

SBI is the most used lender for education loans in India, including for MBBS abroad.

Products:

- SBI Student Loan Scheme: Up to ₹20L without collateral for approved institutions; up to ₹1.5 crore with collateral for international programs at select institutions

- SBI Global Ed-Vantage: Specifically designed for overseas education — covers tuition, hostel, travel, equipment, insurance

Interest Rate (as of early 2026):

- Base: Repo rate linked — approximately 9.5–11% per annum

- 0.5% concession for female students

- 1% concession if full interest is paid during moratorium

Moratorium: Course duration + 6 months (or 1 year after getting a job, whichever is earlier)

Collateral requirement:

- Up to ₹7.5L: No collateral (third-party guarantee needed)

- ₹7.5L–₹20L: Third-party guarantee or collateral

- Above ₹20L: Tangible collateral (property, FD, etc.)

What SBI looks for:

- University on NMC approved list — non-negotiable

- NEET scorecard

- University admission letter

- Parent/guardian income documents

- Property papers (if collateral loan)

Practical note: SBI branches vary significantly in their familiarity with MBBS abroad loans. Urban branches (especially those with education loan desks) are more experienced. If the branch officer says "we don't do this," escalate to the branch manager or visit a different branch.

Bank of Baroda (BoB)

Products:

- Baroda Education Loan (Abroad): Covers NMC-recognized foreign universities; up to ₹80L with collateral

- Baroda Vidya / Baroda Gyan: For select listed institutions — may not directly cover all MBBS abroad universities; ask specifically

Interest Rate: Approximately 10–11.5% p.a. (varies with credit profile and collateral)

Moratorium: Course duration + 12 months

Key feature: BoB has a formal List of Premier Foreign Institutes (LPFI) — universities on this list get preferred processing. Most Kazakhstan, Georgia, Russia universities are not on LPFI, but loans are still available — they are processed as "other approved institutions."

Punjab National Bank (PNB)

PNB Udaan: Education loan for overseas studies

- Up to ₹20L for approved institutions

- Collateral required above ₹7.5L

- Interest rate: 10–11.5% p.a.

- Moratorium: Course + 12 months

Note: PNB's processing for MBBS abroad can be slower than SBI or BoB. Follow up actively.

HDFC Credila (Private Lender)

HDFC Credila is a dedicated education loan NBFC and often faster in processing than public sector banks.

Loan amount: Up to ₹1 crore (subject to creditworthiness and collateral) Interest rate: 11–13% p.a. (higher than PSBs) Collateral: Required above ₹10L Processing time: 7–15 business days (significantly faster than PSBs) Moratorium: Course duration + 6 months

Advantage over PSBs: More flexible in terms of documents approved institutions; faster; can be processed online with less branch friction. The trade-off is a higher interest rate.

Avanse Financial Services

Another dedicated education loan NBFC.

- Loan amount: ₹10L–₹75L for overseas MBBS

- Interest rate: 12–14% p.a.

- Moratorium: Course + 12 months

- Strength: More flexible on institution type; will consider NMC-listed universities more readily than some PSBs

InCred and Propelld

Emerging education loan fintech platforms. Useful for students who cannot access collateral-based loans and need unsecured options.

- Loan amounts typically ₹5L–₹30L

- Interest: 13–18% p.a.

- No collateral for smaller amounts — income-based approval on co-applicant

- Best used for top-up financing, not as primary loan for MBBS abroad

What Education Loans Cover for MBBS Abroad

Most bank education loans for overseas study cover:

| Covered | Usually Not Covered |

|---|---|

| Tuition fees | Personal expenses (food, clothing) |

| University hostel fees | Foreign travel spending |

| Exam/library/lab fees | One-time setup costs |

| Round-trip airfare (capped) | Luxury accommodation |

| Purchase of laptop/equipment (capped) | |

| Study insurance | |

| Caution deposit (refundable) |

Practical implication: Your education loan covers the core institutional costs. You still need family funds or savings for daily food expenses, personal items, and the first-year setup costs.

How Much Should You Borrow?

A common mistake is borrowing the maximum available and then struggling with EMI after graduation. Model your borrowing precisely.

Step 1: Calculate total tuition + hostel over 6 years (get exact figures from university)

Step 2: Calculate flights + insurance + exam fees

Step 3: Estimate family contribution for food and personal expenses

Step 4: Borrow: (Step 1 + Step 2) minus family contribution

Example for KazNMU Almaty:

- Tuition (6Y): ₹30L

- Hostel (6Y): ₹6.6L

- Flights + insurance + fees: ₹5L

- Subtotal institutional costs: ₹41.6L

- Family contribution for food + personal (6Y): ₹15L

- Loan amount to borrow: ₹41.6L

Interest During the Moratorium Period

During the course (moratorium), interest accrues on the disbursed amount even though no EMI is paid. This is called simple interest during moratorium in most PSB schemes.

Example (₹40L loan at 10% p.a.):

- Monthly interest during moratorium: ₹40L × 10% / 12 = ₹33,333/month

- Over 6-year course: ₹33,333 × 72 = ₹24L of interest accrues

- Total amount owed at end of moratorium: ₹40L + ₹24L = ₹64L

This is the principal on which EMI is calculated. If your repayment tenure is 10 years post-moratorium, your EMI on ₹64L at 10% is approximately ₹84,000/month.

The case for paying interest during moratorium: If you pay the monthly simple interest (₹33,333 in the above example) during your 6 years, you save ₹24L in accrued interest and your EMI burden post-graduation is significantly lower. SBI offers a 1% interest rate reduction as an incentive to pay during moratorium.

Collateral: What Banks Accept

For loans above ₹7.5–10L (which covers almost all MBBS abroad cases), banks require:

Immovable property (most common):

- Residential or commercial property in parent/guardian name

- Market value must typically be 1.25–1.5× the loan amount

- Clear title (no disputes, no encumbrance)

- Property in the city/district where the bank branch operates is preferred

Fixed Deposits:

- FD with the lending bank can be pledged

- 100% of FD value can be leveraged

Life Insurance Policy:

- Surrender value must cover loan amount

- Term insurance is not accepted; endowment/whole life policies with surrender value work

Liquid Securities (NSC, KVP, etc.): Accepted at many PSBs

Government Securities: Accepted

If you have no collateral: Some banks offer third-party guarantee (a guarantor with property or income) in lieu of direct collateral. Private lenders like Avanse and Propelld offer partial unsecured options at higher rates.

Step-by-Step Application Process

Step 1: Confirm University NMC Status

Before approaching any bank, download the current NMC approved list and confirm your university is listed. Bring a printout.

Step 2: Get the University Documents

- Admission/Offer Letter (official, on university letterhead)

- Fee structure for all 6 years (or per year)

- Hostel cost breakdown

- University WDOMS listing reference (for bank verification purposes)

Step 3: Prepare Co-applicant Documents

- PAN card

- Aadhaar card

- Last 3 years ITR (Income Tax Returns)

- Last 6 months bank statements

- Salary slips (if salaried) or business proof (if self-employed)

- Property documents (for collateral loan)

Step 4: Prepare Student Documents

- Class 10 and 12 mark sheets and certificates

- NEET scorecard

- Passport (valid for 6+ years)

- NMC eligibility certificate (if already obtained)

- University offer/admission letter

- Passport-size photographs

Step 5: Apply at Bank

Visit the education loan desk. Submit documents. Bank will conduct verification (property valuation if collateral is involved — typically 2–3 weeks).

Step 6: Sanction Letter

Received after approval. This is what you show to the university for installment payment planning.

Step 7: First Disbursement

Banks typically disburse directly to the university's bank account, not to the student. Coordinate university banking details with your bank before departure.

Step 8: Annual Renewal

Education loans for 6-year programs are renewed annually. You provide proof of progress (university mark sheets or attendance certificates) to continue disbursements each year.

Tax Benefits on Education Loan

Under Section 80E of the Income Tax Act, the interest paid on education loans is fully deductible from taxable income — for a maximum of 8 years starting from the year you begin repayment.

This applies to loans taken for higher education (including MBBS abroad) and is available to the student or parent repaying the loan. There is no cap on the interest amount deducted.

In practice: After returning and starting practice, if you are repaying ₹40,000/month interest on your education loan, the annual ₹4.8L interest is fully deductible from your income under Section 80E. At a 30% tax bracket, this saves ₹1.44L/year in tax.

Frequently Asked Questions

Which bank is best for education loan for MBBS abroad? SBI is the most accessible for most students due to its branch network and familiarity with MBBS abroad cases. For faster processing, HDFC Credila is the private sector alternative. For higher loan amounts, Bank of Baroda or SBI's Global Ed-Vantage scheme.

What is the maximum education loan for MBBS abroad? SBI's Global Ed-Vantage offers up to ₹1.5 crore for overseas programs with collateral. In practice, most MBBS abroad loans are processed in the ₹30–60L range.

Can I get an education loan without collateral for MBBS abroad? Loans above ₹7.5L without collateral are rare from PSBs. Private lenders (InCred, Propelld) offer unsecured loans up to ₹20–30L at higher interest rates.

Do banks verify NMC recognition before the loan? Yes — as standard practice. This is one reason why enrolling in a non-NMC-recognized university creates problems: you will not be able to get an education loan, which is a clear warning signal.

When does loan repayment start? Most education loans have a moratorium covering the course duration plus 6–12 months. Repayment (EMI) starts after the moratorium period ends.

Can the loan cover NExT coaching fees after return? No — post-graduation coaching is not covered under standard education loan terms. Plan separately for ₹2–4L for NExT preparation.

What if I don't clear NExT and can't repay the loan? Loan defaults are reported to CIBIL and affect your credit score. If you fail NExT and cannot practice, contact the bank proactively to explore restructuring options — banks have NPA (non-performing asset) resolution processes. Prevention is better: prepare systematically for NExT from Year 1 to avoid this scenario.

Final Checklist Before You Apply

- University confirmed on NMC approved list (nmc.org.in — current year)

- NEET scorecard obtained and percentile noted

- University fee structure obtained in writing

- Co-applicant income and property documents compiled

- Bank branch with education loan desk identified

- Collateral property valued or FD amount confirmed

- Target loan amount calculated (institutional costs only)

- Interest-during-moratorium payment plan discussed with family

Getting the loan sanctioned before departure gives you negotiating power with the university on payment schedules and removes the financial anxiety that derails academic performance in Year 1.